An Environmentally Friendly Vehicle Tax System For Sri Lanka

Lal de Mel

There were many complaints in the news media regarding the increase in the Excise Duty of Toyota Prius cars which are used by most taxi companies for the transport of tourists from the airport, because of the high fuel efficiency, internationally accepted safety standards and the long term durability of the vehicle. When a former Minister now representing the joint opposition made an allegation that the duties of vehicles were revised recently to please the Indian authorities, I decided to carry out a study of the Excise Duty structure of motor cars.

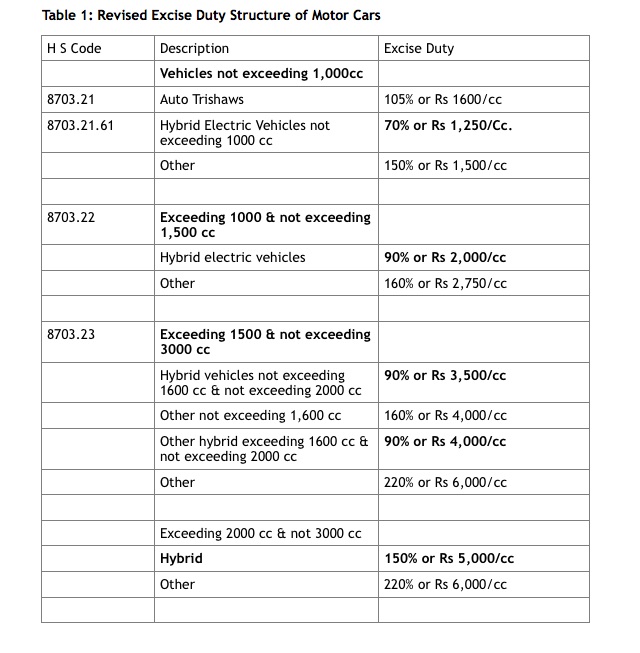

Dr R H S Samaratunga, the Secretary to the Ministry of Finance headed the Trade &Tariff department of the Ministry of Finance from the time the Tariff Committee headed by Mr Nihal Jinasena was replaced by the Trade & Tariff Cluster of the National Council for Economic Development (NCED) and the Transport Cluster of NCED. This was during the time of President Kumaratunga. Professor Amal Kumarage of the Moratuwa University was appointed as the Co-chair of the Transport Cluster with the responsibility of planning the transport strategy and the vehicle tariffs. The writer was appointed as the Co-chair of the Trade & Tariff Cluster with the responsibility of rationalising the tariffs to three bands and introducing additional tariffs to protect local producers as well as the consumers. Dr Samaratunga was responsible for submitting the recommendations for implementation to the Secretary to the Treasury. Dr Samaratunga was a very intelligent and hardworking person with high integrity. The rational vehicle excise duty structure in Table 1 shows that there is no bias in this duty structure.

Dr R H S Samaratunga, the Secretary to the Ministry of Finance headed the Trade &Tariff department of the Ministry of Finance from the time the Tariff Committee headed by Mr Nihal Jinasena was replaced by the Trade & Tariff Cluster of the National Council for Economic Development (NCED) and the Transport Cluster of NCED. This was during the time of President Kumaratunga. Professor Amal Kumarage of the Moratuwa University was appointed as the Co-chair of the Transport Cluster with the responsibility of planning the transport strategy and the vehicle tariffs. The writer was appointed as the Co-chair of the Trade & Tariff Cluster with the responsibility of rationalising the tariffs to three bands and introducing additional tariffs to protect local producers as well as the consumers. Dr Samaratunga was responsible for submitting the recommendations for implementation to the Secretary to the Treasury. Dr Samaratunga was a very intelligent and hardworking person with high integrity. The rational vehicle excise duty structure in Table 1 shows that there is no bias in this duty structure.

The term Excise Duty on vehicles implies that it is a charge levied because of the environmental impact of the particular vehicle. The current Excise Duty structure shown in table 1 appears to be rational, if the emissions are directly related to the engine capacity. This assumption was correct twenty years ago before the launch of energy efficient hybrid motor vehicles. The weakness of the duty structure is in basing the excise duties of hybrid vehicles on engine capacity, rather than the certified fuel efficiency, which is directly proportional to the carbon dioxide emissions.